I asked for “full qqq list alphabetical order” in Googles search page. The google result is as follows:

A full alphabetical list of all QQQ holdings is not publicly available in a single source, as the list changes and contains over 100 companies. However, you can find a list of the top holdings, which are all technology and growth-oriented companies, on the Invesco website.

Seriously how can that be? Well I know the cure, I’ll produce it here and then I’ll search it later and boom I will have fixed Google!

Now that you have seen the list of the QQQ in alphabetical order as of 12/4/2025, please note that I did not include MSTR (Strategy Inc.). Personally I just can’t invest in a company that owns bitcoin, like that’s it. I could own bitcoin if I wanted, why would I invest in a company that does that for me?

After seeing another Ozempic comerical, I found myself wondering how the US would change if this drug or another drug could cut the rate of obesity in the US by 10%. Now why 10%, no reason, just had to start somewhere. If you ever look at old photos, like the one below taken right after World War 2, Americans used to be much smaller.

The increase in BMI values continued throughout the 20th century, especially after World War II. Nationwide surveys conducted by the National Institutes of Health since the early 1960s show that US obesity rates have tripled over the last 60 years, from 13% in 1960-1962 to 43% in 2017-2018. Severe obesity, also known as morbid obesity, has risen tenfold, from less than 1% to nearly 10%. Childhood obesity rates have also tripled, from 5% in the early 1970s to more than 19% by March 2020.

So, if you look at old photos, and look for any easy to find studies, one will quickly figure out that Americans are much larger now than they had been in the past. A 10% reduction in obesity due to miracle drugs isn’t far fetched, so is it something that should be captured in our expectations of growth when we model a Discounted Cash Flow analysis of a health care practice?

In case you haven’t heard, many people take Ozempic, for the side effect of losing weight that was discovered, it was actually designed to treat type 2 diabetes and reduce the risk of cardiovascular events. It belongs to a class of drugs called glucagon-like peptide-1 (GLP-1) receptor agonists, which stimulate the production of insulin and lower blood sugar levels. Ozempic also has an effect on weight loss, as it reduces appetite and slows down gastric emptying.

A recent study published in the New England Journal of Medicine showed that Ozempic, when given at a higher dose than usual, led to an average weight loss of 14.9% over 68 weeks in people with obesity and without diabetes. This is a significant result, as it is comparable to the weight loss achieved by some bariatric surgeries.

But what would happen to the health care revenue expectations if Ozempic lowered obesity in the US by 10%? Obesity is a major risk factor for many chronic diseases, such as diabetes, heart disease, stroke, cancer, and arthritis. It is estimated that obesity costs the US health care system about $147 billion per year, or 10% of total medical spending. If Ozempic could reduce obesity by 10%, it could potentially save $14.7 billion per year in health care costs.

However, this is a simplistic calculation that does not take into account other factors, such as the cost of Ozempic itself, the side effects and complications of the drug, the adherence and compliance of the patients, the availability and accessibility of the drug, and the impact on other health outcomes and quality of life. Moreover, obesity is a complex and multifactorial condition that requires a comprehensive and holistic approach, involving not only pharmacological interventions but also lifestyle changes, behavioral modifications, psychological support, and environmental and policy interventions.

Therefore, while Ozempic may be a promising option for some people with obesity who need additional help to lose weight, it is not a magic bullet that can solve the obesity epidemic in the US. The health care revenue expectations from Ozempic may depend on how well it is integrated into a broader and more sustainable strategy to prevent and treat obesity and its related complications.

Is it time to lower our expectations on the growth of health care revenue going forward, or is it too early to declare a magic pill for obesity is here?

The Headline today was that MGM stock was up after backing out of a deal to acquire Entain. Why would the value of MGM go up in this situation? Well, find out the difference between fair market value and investment (or strategic) value in the video below.

Also, with speculation that Trump will start a media company, find out if the same principles would apply.

The Cares act, or short for the “Coronavirus Aid, Relief, 2 and Economic Security Act’’. Was just passed at the end of March 2020 and most Americans are expecting to receive a check of $1,200 from the government in the next few weeks. However, if you make more than $75,000 or $150,000 for a married couple you may receive a reduced amount or nothing at all. Don’t panic, if you are a high earner or a small business owner you may have a chance to get far more than the rest of America buy using the TITLE I—KEEPING AMERICAN WORKERS PAID AND EMPLOYED ACT portion of the bill. In essence, one must take out an SBA 7(a) loan from a bank, keep payroll similar to the level that you had in the past and then apply for loan forgiveness. Sounds easy right? Well let’s dig in. If you prefer watching, I have a video that is about 25 minutes that goes into the bill below. Or if you prefer reading the entire CARES bill can be found here.

Want the TLDR?

If you have a small business or receive a 1099-Misc, earn less than $100,000 per year, then you may be eligible for a SBA 7(a) loan which is forgivable AKA FREE MONEY, and much more than the $1,200 that the media keeps talking about.

CARES Act Small Business Loans VIDEO

The SBA 7(a) program and the CARES Act

The Cares act is going to force small business owners to jump through some hoops, but the rewards are going to be huge and hopefully, will help your business survive in the covid-19 era.

Let’s start with who is eligible. If you work for someone as an employee, there is no reason to keep reading, it will only make you jealous as you learn how much more the owner of your company will get. Now if you are the owner of a S-corp, or a C-corporation, and LLC, Partnership, sole proprietor, or an independent contractor keep reading.

Check your tax returns do you normally receive a 1099-misc? As a small business owner do you issue yourself a W-2 that is under $100,000? If so keep reading.

Here is the Title of the first section of the Cares bill:

DIVISION A—KEEPING WORKERS PAID AND EMPLOYED, HEALTH CARE SYSTEM ENHANCEMENTS, AND ECONOMIC STABILIZATION TITLE I—KEEPING AMERICAN WORKERS PAID AND EMPLOYED ACT

The very first words in the first section are KEEPING WORKERS PAID AND EMPLOYED. The bill is clearly designed to keep the unemployment stats down by keeping people on the payroll during this corona virus crisis. The way to do this is to provide small loans (up to $10,000,000) to small businesses, which will be forgivable if the business owners maintain their payroll. Sounds easy right? Well let’s dig into some of the key provisions.

IN GENERAL.—Section 7(a) of the Small Business Act (15 U.S.C. 636(a)) is amended—

Again in the beginning, they are stating that the program that will be used for this stimulus package is the SBA Section 7(a) loan. If you walk into a bank and they offer you another solution it may not be FORGIVABLE, which is the key. You are searching for a solution that is also FREE MONEY, as long as you play by the rules. The first thing that a small business owner needs to do is look at their payroll for the last 12 months, here is the language around that: the term ‘payroll costs’ ‘‘(I) means— ‘‘(aa) the sum of payments of any compensation with respect to employees that is a— ‘‘(AA) salary, wage, commission, or similar compensation; ‘‘(BB) payment of cash tip or equivalent; ‘‘(CC) payment for vacation, parental, family, medical, or sick leave;

†HR 748 EAS ‘‘(DD) allowance for dismissal or separation; ‘‘(EE) payment required for the provisions of group health care benefits, including insurance premiums; ‘‘(FF) payment of any retirement benefit; or ‘‘(GG) payment of State or local tax assessed on the compensation of employees; and ‘‘(bb) the sum of payments of any compensation to or income of a sole proprietor or independent contractor that is a wage, commission, income, net earnings from self-employment, or similar compensation and that is in an amount that is not more than $100,000 in 1 year, as prorated for the covered period;

Notice section (bb) above which allows for independent contractors (think UBER drivers) and sole proprietors (think a one person tax firm, or a small restaurant). This was a provision that they put in the the last minute as they realized that the backbone of our economy would not be able to survive off of the $1,200 as they probably wouldn’t also be covered by unemployment insurance. As a side note, I’m not sure if I could “fire” myself from my one person S-Corporation, and then claim unemployment insurance. Maybe I could but the way that unemployment insurance can scale back your check if your business gets some income in the door, I don’t think I would be eligible to receive anything from that program.

So the government was looking out for those of us who run small businesses, in fact, I argue that they are doing everything possible to keep small businesses alive with these provisions.

Who isn’t elibible:

shall not include— †HR 748 EAS ‘‘(aa) the compensation of an individual employee in excess of an annual salary of $100,000, as prorated for the covered period;

any compensation of an employee whose principal place of residence is outside of the United States;

Seems pretty straight forward, wages need to be under $100,000 and you need to live in the US to be eligible.

business concern employs not more than the greater of— ‘‘(I) 500 employees;

I know that a larger small business with say 400 employees could use this rather than laying off their work force, but I’m not sure it actually pencils out to keep people on the payroll if the stay at home type of shut downs extend into the summer.

IN GENERAL.—During the covered period, individuals who operate under a sole proprietorship or as an independent contractor and eligible self-employed individuals shall be eligible to receive a covered loan.

This section further notes that independent contractors or GIG economy employees are covered.

MAXIMUM LOAN AMOUNT.—During the covered period, with respect to a covered loan, the maximum loan amount shall be the lesser of— ‘‘(i)(I) the sum of— ‘‘(aa) the product obtained by multiplying— ‘‘(AA) the average total monthly payments by the applicant for payroll costs incurred during the 1-year period before the date on which the loan is made, except that, in the case of an applicant that is seasonal employer, as determined by the Administrator, the average total monthly payments for payroll shall be for the 12 week period beginning February 15, 2019, or at the election of the eligible

†HR 748 EAS

ent, March 1, 2019, and ending 1 June 30, 2019; by 2 ‘‘(BB) 2.5; and ‘‘(bb) the outstanding amount of a loan under subsection (b)(2) that was made during the period beginning on January 31, 2020 and ending on the date on which covered loans are made available to be refinanced under the covered loan; or ‘‘(II) if requested by an otherwise eligible recipient that was not in business during the period beginning on February 15, 13 2019 and ending on June 30, 2019, the sum of— ‘‘(aa) the product obtained by multiplying ‘‘(AA) the average total monthly payments by the applicant for payroll costs incurred 20 during the period beginning on January 1, 2020 and ending on February 29, 2020; by ‘‘(BB) 2.5; and 24

19

†HR 748 EAS

‘‘(bb) the outstanding amount of a loan under subsection (b)(2) that was made during the period beginning on January 31, 2020 and ending on the date on which covered loans are made available to be refinanced under the covered loan; or ‘‘(ii) $10,000,000.

WOW that’s a lot of hard to understand legalese isn’t it? I’m pretty sure that it says that you can take your average monthly salary (as long as that yearly salary is less than $100,000) and multiply that by 2.5 and ask for a SBA 7(a) loan in that amount to cover payroll.

Can I use my SBA 7(a) loan for personal expenses?

No!!! Don’t go buy a boat or a luxury vacation (oh wait they don’t have those anymore do they?) Here are the acceptable uses of these loans: ALLOWABLE USES OF COVERED LOANS.— ‘‘(i) IN GENERAL.—During the covered period, an eligible recipient may, in addition to the allowable uses of a loan made under this subsection, use the proceeds of the covered loan for— ‘‘(I) payroll costs; ‘‘(II) costs related to the continuation of group health care benefits during periods of paid sick, medical, or family leave, and insurance premiums; ‘‘(III) employee salaries, commissions, or similar compensations; ‘‘(IV) payments of interest on any mortgage obligation (which shall not

†HR 748 EAS

include any prepayment of or payment of principal on a mortgage obligation); ‘‘(V) rent (including rent under a lease agreement); ‘‘(VI) utilities; and ‘‘(VII) interest on any other debt obligations that were incurred before the covered period.

What do you have to pledge to get a Cares SBA loan?

BORROWER REQUIREMENTS.— ‘‘(i) CERTIFICATION.—An eligible recipient applying for a covered loan shall make a good faith certification— ‘‘(I) that the uncertainty of current economic conditions makes necessary the loan request to support the ongoing operations of the eligible recipient; ‘‘(II) acknowledging that funds will be used to retain workers and maintain payroll or make mortgage payments, lease payments, and utility payments; ‘‘(III) that the eligible recipient does not have an application pending for a loan under this subsection for the same purpose and duplicative of

†HR 748 EAS

amounts applied for or received under a covered loan; and ‘‘(IV) during the period beginning on February 15, 2020 and ending on December 31, 2020, that the eligible recipient has not received amounts under this subsection for the same purpose and duplicative of amounts applied for or received under a covered loan.

How Much does a Cares Act Loan Cost?

Should be ZERO here is the way that it is worded:

FEE WAIVER.—During the covered period, with respect to a covered loan ‘‘(i) in lieu of the fee otherwise applicable under paragraph (23)(A), the Administrator shall collect no fee; and ‘‘(ii) in lieu of the fee otherwise applicable under paragraph (18)(A), the Administrator shall collect no fee.

Don’t sleep on this section, it is saying that you are agreeing to the terms that they are laying out and pledging to play by their rules by basically keeping your payroll up and not spending the money on a new RV.

They also require no collateral and no personal guarantee (WHICH IS HUGE!!!):

‘‘(J) WAIVER OF PERSONAL GUARANTEE REQUIREMENT.—During the covered period, with respect to a covered loan—

†HR 748 EAS ‘‘(i) no personal guarantee shall be required for the covered loan; and ‘‘(ii) no collateral shall be required for the covered loan.

What are the Terms of a SBA 7(a) CARES Loan?

‘‘(ii) the covered loan shall have a maximum maturity of 10 years from the date on which the borrower applies for loan forgiveness under that section. ‘‘(L) INTEREST RATE REQUIREMENTS.—A covered loan shall bear an interest rate not to exceed 4 percent.

So a 10 year loan with a max 4% interest rate. I have had some clients get 3% loans in early March so you may get lucky and get a sub 4% loan.

Payments to this loan may be deferred for up to a year: the Administrator shall exercise the authority to purchase the loan so that the impacted borrower may receive a deferral for a period of not less than 6 months, including payment of principal, interest, and fees, and not more than 1 year.

This loan also has no prepayment penalty: ‘‘(R) WAIVER OF PREPAYMENT PENALTY.—Notwithstanding any other provision of law, there shall be no prepayment penalty for any payment made on a covered loan.’’.

You Must Demonstrate Hardship from Covid-19 to be Eligible

I can’t imagine that it is too hard to demonstrate that Covid-19 damaged your small business. For me I’ll just point to section III part c below. (a) DEFINITIONS.—In this section— (1) the term ‘‘covered small business concern’’ means a small business concern that has experienced, as a result of COVID–19— (A) supply chain disruptions, including changes in(i) quantity and lead time, including the number of shipments of components and delays in shipments;

†HR 748 EAS

(ii) quality, including shortages in supply for quality control reasons; and (iii) technology, including a com-3 promised payment network; (B) staffing challenges; (C) a decrease in gross receipts or customers; or (D) a closure;

My business has been completely decimated by this corona virus. The majority of my clients are dentists and the ADA (american dental association) has basically closed down dental practices. Which makes perfect sense as they can conserve PPE and not get exposed to potentially sick patients.

Do I Have To Pay Back My SBA 7(a) CARES loan?

If you can maintain your payroll then NO you don’t have to pay back the loan after you apply for loan forgiveness AKA FREE MONEY! So if you play by the rules and spirit of the CARES act Small Business owners can get far more FREE MONEY than the $1,200 that you see all over the media. SEC. 1106. LOAN FORGIVENESS. (a) DEFINITIONS.—In this section— (1) the term ‘‘covered loan’’ means a loan guaranteed under paragraph (36) of section 7(a) of the Small Business Act (15 U.S.C. 636(a)), as added by section 1102; (2) the term ‘‘covered mortgage obligation’’ means any indebtedness or debt instrument incurred in the ordinary course of business that— (A) is a liability of the borrower; (B) is a mortgage on real or personal property; and (C) was incurred before February 15, 2020; (3) the term ‘‘covered period’’ means the 8-week period beginning on the date of the origination of a covered loan; (4) the term ‘‘covered rent obligation’’ means rent obligated under a leasing agreement in force before February 15, 2020; (5) the term ‘‘covered utility payment’’ means payment for a service for the distribution of electricity, gas, water, transportation, telephone, or internet access for which service began before February 15, 2 2020; (6) the term ‘‘eligible recipient’’ means the recipient of a covered loan; (7) the term ‘‘expected forgiveness amount’’ means the amount of principal that a lender reasonably expects a borrower to expend during the covered period on the sum of any— (A) payroll costs; (B) payments of interest on any covered mortgage obligation (which shall not include any prepayment of or payment of principal on a covered mortgage obligation); (C) payments on any covered rent obligation; and (D) covered utility payments; and(8) the term ‘‘payroll costs’’ has the meaning given that term in paragraph (36) of section 7(a) of the Small Business Act (15 U.S.C. 636(a)), as added by section 1102 of this Act. (b) FORGIVENESS.—An eligible recipient shall be eligible for forgiveness of indebtedness on a covered loan in an amount equal to the sum of the following costs incurred and payments made during the covered period:

(1) Payroll costs. (2) Any payment of interest on any covered mortgage obligation (which shall not include any prepayment of or payment of principal on a covered mortgage obligation). (3) Any payment on any covered rent obligation. (4) Any covered utility payment. (c) TREATMENT OF AMOUNTS FORGIVEN.— (1) IN GENERAL.—Amounts which have been for-given under this section shall be considered canceled indebtedness by a lender authorized under section 7(a) of the Small Business Act (15 U.S.C. 636(a)). (2) PURCHASE OF GUARANTEES.—For purposes of the purchase of the guarantee for a covered loan by the Administrator, amounts which are forgiven under this section shall be treated in accordance with the procedures that are otherwise applicable to a loan guaranteed under section 7(a) of the Small Business Act (15 U.S.C. 636(a)). (3) REMITTANCE.—Not later than 90 days after the date on which the amount of forgiveness under this section is determined, the Administrator shall remit to the lender an amount equal to the amount of forgiveness, plus any interest accrued through the date of payment.

Are there Limits to the Forgiveness?

Yes but they are pretty logical, don’t cut your staff or the forgiveness level will be cut. Don’t expect to get more than what they loan you… Duh.. LIMITS ON AMOUNT OF FORGIVENESS.— (1) AMOUNT MAY NOT EXCEED PRINCIPAL.—The amount of loan forgiveness under this section shall

not exceed the principal amount of the financing made available under the applicable covered loan. (2) REDUCTION BASED ON REDUCTION IN NUMBER OF EMPLOYEES.— (A) IN GENERAL.—The amount of loan forgiveness under this section shall be reduced, but not increased, by multiplying the amount described in subsection (b) by the quotient obtained by dividing— (i) the average number of full-time equivalent employees per month employed by the eligible recipient during the covered period; by (ii)(I) at the election of the borrower— (aa) the average number of full- time equivalent employees per month employed by the eligible recipient during the period beginning on February 15, 2019 and ending on June 30, 2019; or (bb) the average number of full- time equivalent employees per month employed by the eligible recipient during the period beginning on January 24

, 2020 and ending on February 29, 1 2020; or (II) in the case of an eligible recipient that is seasonal employer, as determined by the Administrator, the average number of full-time equivalent employees per month employed by the eligible recipient during the period beginning on February 15, 2019 and ending on June 30, 2019. (B) CALCULATION OF AVERAGE NUMBER OF EMPLOYEES.—For purposes of subparagraph (A), the average number of full-time equivalent employees shall be determined by calculating the average number of full-time equivalent employees for each pay period falling within a month. (3) REDUCTION RELATING TO SALARY AND WAGES.— (A) IN GENERAL.—The amount of loan forgiveness under this section shall be reduced by the amount of any reduction in total salary or wages of any employee described in subparagraph (B) during the covered period that is in excess of 25 percent of the total salary or wages of the employee during the most recent full quarter during which the employee was employed before the covered period. (B) EMPLOYEES DESCRIBED.—An employee described in this subparagraph is any employee who did not receive, during any single pay period during 2019, wages or salary at an annualized rate of pay in an amount more than $100,000. (4) TIPPED WORKERS.—An eligible recipient with tipped employees described in section 3(m)(2)(A) of the Fair Labor Standards Act of 1938 (29 U.S.C. 203(m)(2)(A)) may receive forgiveness for additional wages paid to those employees. (5) EXEMPTION FOR RE-HIRES.— (A) IN GENERAL.—In a circumstance described in subparagraph (B), the amount of loan forgiveness under this section shall be determined without regard to a reduction in the number of 18 full-time equivalent employees of an eligible recipient or a reduction in the salary of 1 or more employees of the eligible recipient, as applicable, during the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of enactment of this Act.

(B) CIRCUMSTANCES.—A circumstance described in this subparagraph is a circumstance— (i) in which— (I) during the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of enactment of this Act, there is a reduction, as compared to February 15, 2020, in the number of full-time equivalent employees of an eligible recipient; and (II) not later than June 30, 2020, the eligible employer has eliminated the reduction in the number of full- time equivalent employees; (ii) in which— (I) during the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of enactment of this Act, there is a reduction, as compared to February 15, 2020, in the salary or wages of 1 or more employees of the eligible recipient; and

(II) not later than June 30, 2020, the eligible employer has eliminated the reduction in the salary or wages of such employees; or (iii) in which the events described in clause (i) and (ii) occur. (6) EXEMPTIONS.—The Administrator and the Secretary of the Treasury may prescribe regulations granting de minimis exemptions from the requirements under this subsection. (e) APPLICATION.—An eligible recipient seeking loan forgiveness under this section shall submit to the lender that is servicing the covered loan an application, which shall include— (1) documentation verifying the number of full- time equivalent employees on payroll and pay rates for the periods described in subsection (d), including— (A) payroll tax filings reported to the Internal Revenue Service; and (B) State income, payroll, and unemployment insurance filings; (2) documentation, including cancelled checks, payment receipts, transcripts of accounts, or other documents verifying payments on covered mortgage

obligations, payments on covered lease obligations, and covered utility payments; (3) a certification from a representative of the eligible recipient authorized to make such certifications that— (A) the documentation presented is true and correct; and (B) the amount for which forgiveness is requested was used to retain employees, make interest payments on a covered mortgage obligation, make payments on a covered rent obligation, or make covered utility payments; and (4) any other documentation the Administrator determines necessary. (f) PROHIBITION ON FORGIVENESS WITHOUT DOCUMENTATION.—No eligible recipient shall receive forgiveness under this section without submitting to the lender that is servicing the covered loan the documentation required under subsection (e). (g) DECISION.—Not later than 60 days after the date on which a lender receives an application for loan forgiveness under this section from an eligible recipient, the lender shall issue a decision on the an application. (h) HOLD HARMLESS.—If a lender has received the documentation required under this section from an eligible

recipient attesting that the eligible recipient has accurately verified the payments for payroll costs, payments on covered mortgage obligations, payments on covered lease obligations, or covered utility payments during covered period— (1) an enforcement action may not be taken against the lender under section 47(e) of the Small Business Act (15 U.S.C. 657t(e)) relating to loan forgiveness for the payments for payroll costs, payments on covered mortgage obligations, payments on covered lease obligations, or covered utility payments, as the case may be; and (2) the lender shall not be subject to any penalties by the Administrator relating to loan forgiveness for the payments for payroll costs, payments on covered mortgage obligations, payments on covered lease obligations, or covered utility payments, as the case may be. (i) TAXABILITY.—For purposes of the Internal Revenue Code of 1986, any amount which (but for this sub-section) would be includible in gross income of the eligible recipient by reason of forgiveness described in subsection (b) shall be excluded from gross income. (j) RULE OF CONSTRUCTION.—The cancellation of indebtedness on a covered loan under this section shall not

otherwise modify the terms and conditions of the covered loan. (k) REGULATIONS.—Not later than 30 days after the date of enactment of this Act, the Administrator shall issue guidance and regulations implementing this section.

Can you get the $1,200 and get an SBA loan?

If you are in the gig economy, say a lyft or uber driver, I think you are going to be qualified to essentially double dip. The Cares bill allows independent contractors to get the SBA loans, which means that you can get 2.5 times your monthly earnings. If those earnings are less than $100,000 per year it seems likely that you would also qualify for the $1,200 check.

Should I get a CARES SBA Loan for my Small Business?

If you hate FREE MONEY, then no. Otherwise, run to your bank and ask for one, just make sure that you stand 6 feet behind what should be a HUGE LINE!

Do the math on this. Let’s say that you pay a W-2 wage to yourself of $5,000 per month for your small tax preparation business. You can apply to get $12,500 loan at a 4% interest rate that you don’t have to start paying back for at least 6 months, and then if you don’t cut your own wages, you get the entire $12,500 loan forgiven, yes FREE MONEY!!! Way more than you would get with the Trump signed $1,200 checks that the media is so focused on.

Personally, I’m going to go to the bank this morning 3/30/2020 and will update this post with my experience there.

Update 3/30/2020 My First Trip to the Bank

Went to the opening of the nearest bank that I use for my business. They had a line of about 10 of us, spaced out appropriately. Manager comes out and says only 4 people inside at a time. As the gatekeeper she directs people to their destination, first 4 people say teller so she lets them in. I say sba 7 loan. She says oh for the stimulus?

I say yes, she says: “we don’t have that here, you have to apply online.”

So I come home hop on their website, and just like this morning there is no option for a paycheck/Cares loan.

I then search on the web and find the national SBA site, which currently has three sections.

What is it

Who is eligible

Other resources

The other leads you down a rabbit hole to nowhere. AS IN YOU CAN’T CURRENTLY GET A LOAN FOR THIS!!!

Imagine all of the paperwork that needs to be pushed to document and give out these loans. There is no way that our banking infrastructure is set up to do this for awhile. My guess is that links to applications will start showing up by Friday the 3rd of April, but they won’t be able to process it for weeks if you can even get that far.

I received my PPP Loan on May 1

My journey with the Payroll Protection Program is mostly complete. I received my loan on May 1 after the second round of funding. As I’m sure you know the first round was gobbled up by large businesses. After a social backlash for all of the large companies, like the Lakers, Shake shack, etc. the banks started to push out smaller loans.

My understanding is that banks get 1% for huge loans and 5% for micro loans. So if they loan out $10 million they get $100,000 in fees. On a $10,000 loan they are looking at $500.

Assuming it takes say an hour worth of administrative time to deal with the SBA paperwork. Would you rather get paid $500/hour or $100,000?

This is a clear failure in the design of the law that ensured that the big companies got money way before the small companies.

The larger question that taxpayers should ask is: “why are the banks getting paid for this? Why didn’t the SBA just do it all directly?”

I would think that our technology has evolved to the point where paperwork could be filled out online and that the government should know enough about all of the companies from their tax records, 1120’s, schedule c, 940-941 that they should have been able to do the legwork rather than giving away all of that money to banks.

Not investment advice, but I’m thinking that giving all of this highly profitable business to banks can only be a positive to their share prices.

This post is for discussion purposes only, it is not legal or tax advice. Please consult your legal or tax adviser for full details on how the CARES act will apply to your situation.

Real Estate Appraisers mainly rely on “Market Comps” to derive a value of the property that they are appraising. Business Appraisers are typically more concerned with the amount of cash that flows through a business after all of the other bills are paid. This is the core difference between business appraisals and real estate appraisals, but let’s dig a bit deeper.

How Much Does A House Appraisal Cost?

Expect to pay anywhere from $300 to $750 depending on the size and task that the bank assigns to them. We just purchased a home last week and the lender (Chase) ordered our house appraisal and charged us $500 for it. After it was complete they then tacked on another $250 for Chase to review it. Let’s assume that is the market cost for a formal real estate appraisal in Scottsdale, Arizona. Sometimes the lender will request a “desk review” appraisal. This is where the appraiser checks out the comparable sales in the area and provides a ballpark estimated value. Since the comps are the most important real estate valuation method, this generally leads to similar results as the formal appraisal.

How Much Does A Business Appraisal Cost?

This is a tricky question to answer as businesses are not homogeneous like real estate. Is this a single owner business, or is this a multi-billion dollar business? Does the business have 5 employees or 5,000? What is the purpose of the appraisal? Is this for divorce? A potential sale? Is the bank requesting it? All of those factors come into play, which means that the process of hiring an appraiser typically involves getting bids from a few different companies. Each of those appraisers needs to know what the purpose of the assignment is along with an idea of the complexity of the business structure. He or she would then estimate the amount of hours needed to complete the scope of work and would then prepare a quote for the job. Hourly rates for appraisers are typically in the $200-$500 range depending on the seniority, training and certifications of the appraiser. An appraiser who specializes in family law, and spends a good deal of time in court, will command a higher hourly rate than one who specializes in franchise or restaurant valuations. Knowing an hourly only answers half of the question: How much does an appraisal cost? The other side of the equation is how much time should it take to complete the assignment. Again it is difficult to answer, so I’ll give you a few estimated times for some of the projects that I have worked on during my 20 year career as an appraiser. Dental Practice

Expect a Dental Practice Appraisal to take 10-15 hours to complete.

Restaurant appraisals are on the easier end of the appraisal world so expect around 8-10 hours of work. However, if it is involved in a divorce case, assume double the hours.

Assume that an appraiser needs about 10 hours per appraisal of an optometry clinic. So 20 times 10 is equal to 200 hours for this assignment right? Fortunately, no. Typically, the owner of a business will have consolidated financials so that the appraiser can produce one report that covers the entire business. It will be more work than just a one office clinic, but you could expect that an appraiser could preform the work in about 30-40 hours.

How to Value Real Estate

Real Estate appraisals require state licensed real estate appraisers. They are typically hired by a bank to ensure that the house or commercial property will provide sufficient collateral for a loan. Licensed real estate appraisers use three approaches to value:

Market Approach

Cost Approach

Income Approach

Market Approach

The market approach is heavily favored in Real Estate Appraisal. For the most part houses are homogeneous, land is land and dirt is dirt. Real estate agents always preach location, location, location. What better way to figure out what the location is worth, than looking at the comps to find out what houses in the neighborhood sold for? The market approach allows an appraiser to take certain statistics from nearby house sales and apply them to the house that they are appraising. Statistics that they are looking for are:

Square footage

Number of Bedrooms

Number of Bathrooms

Number of Garage Spots

Is there a Pool, or other upgrades to the backyard?

Has the house been updated recently?

Date Property was Built

Date Property Sold

Price Paid for the Property

Once they have pulled up certain statistics like Price per Square foot, or Price per Bedroom, the appraiser can then apply those metrics to the house they are appraising.

Market Approach Example in Real Estate

In this neighborhood 2 houses have recently sold. Both had the same model of home design (same builder) and are 2,000 sqft. The only difference is that Comp A has recently been upgraded with a new kitchen. Comp B has the same kitchen from when the house was built in 1995. Comp A sold for $600,000 or $300 a sqft. Comp B sold for $560,000 or $280 a sqft.

The appraiser then looks at the condition of the subject house and decides that it also has not been updated since it was built in 1995. The appraiser selects $280 a sqft as a reasonable estimate of the value of the subject house. Knowing that the subject house is 2,500 sqft, the appraiser calculates a value of $700,000 for the subject property.

The appraiser could do the same for many other metrics to get a sense of what the value should be. Backed by a solid statistical database the real estate appraiser is armed with more than enough metrics to provide an appraisal of either a commercial property or a residential one.

Cost Approach

The cost approach in real estate appraisal is pretty straight forward. The appraiser needs to estimate what it would cost to build that structure today. Using data and knowledge of local housing costs per square footage the appraiser can estimate the cost to replace the subject property.

Income Approach in Real Estate

Treating the subject property as an investment yields a different result for an appraiser. The appraiser examines local rent and assumes marketing costs and the time between renters to calculate a value of the rental stream of income to the property. The appraiser can choose to use a gordon growth method or a more complex discounted cash flow method.

How to Value a Business

Business appraisers are not state licensed, in fact there are no licenses for business appraisers in the US. In order to find a qualified appraiser, one needs to examine the credentials of the appraiser. If an appraiser doesn’t have an ASA, CVA, or ABV after their names, they likely wouldn’t pass a Daubert Challenge in court.

Certified Business Valuators follow guidelines called the Uniform Standards of Professional Appraisal Practice (USPAP). Business appraisers typically rely on 3 approaches to value.

Income Approach

Market Approach

Asset Approach

Income Approach in Business Valuation

This approach is the favored approach in business valuation. The appraiser assumes that a hypothetical buyer would come in and purchase the business. This investor uses two things to value the business:

How much profit can they make after paying all the bills and making sure that management is appropriately paid?

How risky is this business compared to all of the other investment choices available?

The appraiser will use statistics to determine an investors required return for different business categories and assign a risk (cap rate or discount rate) to the subject property. The appraiser then needs to examine the business to determine how much cash flow is available to this hypothetical investor. From this point the appraiser can use a capitalization of excess earnings method or a more complicated discounted cash flow method. Using the same growth rate for the business will yield identical results.

Market Approach in Business Valuation

Just like in the real estate example above, the appraiser pulls comps from a database and applies certain metrics to the business. Unfortunately, businesses are not homogeneous and the data sources filled with comps are no where near as good as the data sources that real estate appraisers have access to. Further, only successful businesses sell and make it into the databases. Think about that for a second, if 50% of restaurants fail in the first few years, none of those make it into the database. The same goes for a medical doctor in a small town who simply cleans out his office and retires. By nature the entire database is biased upwards, meaning that any value derived from a market approach is higher than what the value of the business should be.

Many appraisers tend to pull statistics from the selected (filtered) database and apply them to the subject property. I tend to use regression analysis to apply the comps to the subject business.

In the end, business appraisers typically give little to no weight to the results of the market based methods due to the poor data to start with.

Asset Approach in Business Valuation

The asset approach usually does not yield credible results in professional service businesses (accounting firms, doctor’s offices, consulting firms, etc.). The main reason is that professional businesses rely on their employees to turn a profit not expensive machinery.

However, a huge factory relies on equipment and not necessarily people to generate revenue and profits. In businesses that don’t rely on people, an asset approach is an appropriate method to use.

The asset approach involves calculating a market value for all of the plant, property and equipment in use by the company. An appraiser may also consider the brand value of the item that the factory produces and sells.

Business Appraisal Vs. Real Estate Appraisal Conclusion

Business appraisal is:

More complicated

More time consuming

Heavily reliant on the Income Approach

More expensive

Harder to shop for

Not regulated

Businesses are portable, possibly worldwide

Real estate appraisal is:

Less expensive

Local, location, location, location!

Less time consuming

Heavily reliant on Market Based Comps

State Regulated

Easy to shop for (banks select appraisers from a pool)

It is almost tax time, do you know how to report your cryptocurrency gains?

I read a lot of really bad tax advice on various internet forums, like Reddit. The most common myth that I see is that you don’t have to pay taxes on cryptocurrency gains as long as you “never cash out”. Well, that’s simply not true, sorry to break the news to you.

Let’s look at an example of a taxable event:

I purchase a car for $10,000, and own it for over a year. The car becomes extremely popular, since it was featured in the latest blockbuster movie (think the DeLorean). I then sell the car for $20,000 in gold. Was this a taxable event? Of course, I gained $10,000 in value, and the IRS is quite happy for my success. So happy that they remember to send me a bill for capital gains taxes on that $10,000 value. My “problem” is that I have $20,000 worth of gold and I owe the government $1,500 that I had forgotten about. I’m forced to sell a bit of my gold to pay my extra tax bill on 4/17/18.

Now let’s assume that rather than taking gold you accepted $10,000 in Bitcoin and $10,000 in Ripple. Does the IRS think that you made a gain? Yep! Do they want to collect capital gains taxes on the $10,000 increase in value, even though you aren’t actually holding the cash necessary to pay their bill? Yes, if you can’t come up with the US dollars needed to pay your tax bill you will be forced to liquidate part of your crypto portfolio. Now you are forced to make the decision of which coin to sell, you don’t have to sell all of it. Since, they both went up in value since your sale of the car, you are going to have to report a gain on the coin that you sold in order to pay your tax bill for 2017. Don’t worry at least this time you don’t have to pay gains on that sale until 2018.

Here is a nightmare tax scenario for 2018

Did you know that exchanging your Bitcoin for Ethereum and then for Ripple could set off gains in two categories? Let’s say that you bought 1 bitcoin for $1,000. You then traded it for $12,000 in Ethereum. You purchased Ripple with all of your Ethereum 2 weeks later. During that time your Ethereum holdings went up 10%. Guess what, the IRS wants you to report gains on that as well. Imagine that you were new to investing and you didn’t keep records of this, and you did many different similar transactions. You will have a serious issue this April 17th. Rather than digging a hold and sticking your head into it, it is time to start gathering up all of your trading information.

You need to know the cost basis of all of your coins as well as the time that you traded into each position and out of each position. One last thing, the price of your cryptocurrency portfolio could go down when other people are faced with the same problem of having an unexpected tax bill with phantom gains. This will be a major issue that forces many people to liquidate portions of their crypto portfolio at the same time to cover their tax bills.

We can help you sort this out with our Crytpocurrency Valuation Services.

If you had significant gains, or gave away a large amount of cryptocurrency to friends family or charity, you may find your self in search of an IRS qualified appraiser. Look no further, not only do I understand the issues, but I am an IRS qualified appraiser by their definition.

Has earned an appraisal designation from a recognized professional appraisal organization, or has met certain minimum education and experience requirements.

Regularly prepares appraisals for which the individual is paid.

Demonstrates verifiable education and experience in valuing the type of property being appraised.

Has not been prohibited from practicing before the IRS in the last three years

Is not an excluded individual.

As an ASA (Acredited Senior Appraiser with the American Society of Appraisers) I am qualified to do cryptocurrency valuations. Please send an email to ross@medicalvaluations to discuss your cryptocurrency appraisal needs.

I have appraised enough tech businesses in 2017 to cave in to their requests of accepting Bitcoin

It is a bit of a hassle to convert it back to cash, and it is clearly a gamble to hold on to it. However, I would rather accept it than miss out on a potential client. Plus the added benefit to me is that I get to diversify my client portfolio while really increasing the risk of my investment portfolio. A win/win? Probably not, but I would rather make this change than move on and look like a dinosaur.

The transactional fees involved in purchasing things in bitcoin are high and the confirmation times are long. Not good if you are trying to buy gas or pick up a sandwich. However, appraisals take time, and I already pay high transaction fees to use Square as my credit card processing company. So if you find that you are in need of an appraisal and you are sitting on some Bitcoin investments, I’ll accept them for the usual fee. I’ll eat those transactional costs, just like I do with my credit card paying customers.

If you decide to jump on the crypto bandwagon, make sure you keep it safe with a wallet like the Ledger Nano.

I also accept Bitcoin Cash, which is similar, but has lower fees and faster transactions. Contact me to go over the details.

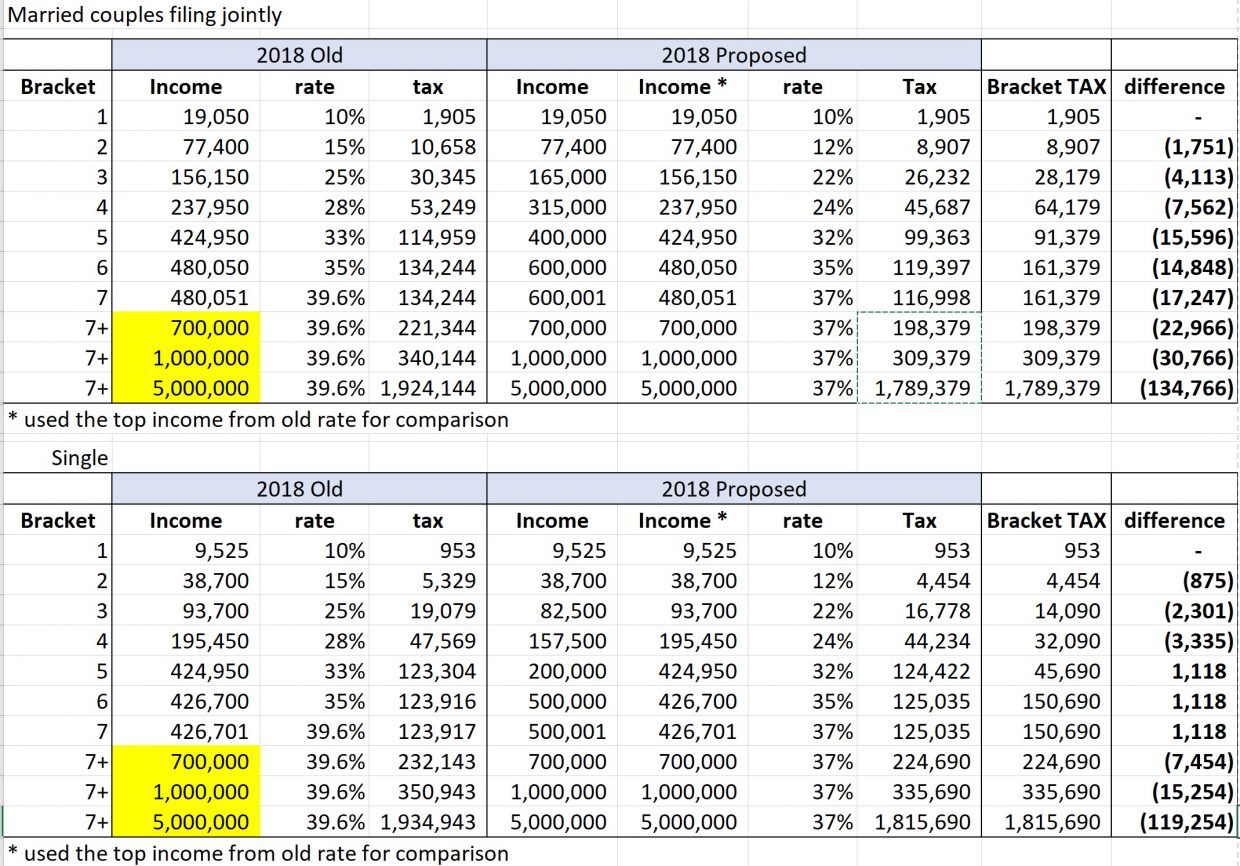

Most people are going to be pleased with the proposed 2018 Tax Brackets

However, there is a “sweet spot” for the government, in the 2018 tax brackets, where some people aren’t going to see a cut. So if you are filing single in 2018, the government may be giving you a little incentive to find a dance partner. Below is a model that I built so that you can see how the different rates stack up. For the single filers, keep your eyes on the old 33%-39.6% rates. In the past they were bunched up together, but now they are proposed to be split up more. Basically, what is happening is that in the old plan for 2018 you would have spent more time in the 33% bracket, and now you are spread into the 35% bracket for longer. Confused? You should be, didn’t President Trump say that we were going to be able to do taxes on a napkin? Well, no surprise it isn’t much less complicated that it has been for the last several decades so here is a model that you can use to see your situation.

If you are one of the lucky filers in the top 1%, you can change the yellow highlighted sections to get a better estimate of your taxes.

I mainly deal with medical professionals so I am going to discuss the married couples filing jointly chart in the top brackets.

What kind of tax savings would an Oral Surgeon, Orthodontist, or Plastic Surgeon see?

When I’m appraising those kinds of medical practices I typically see income in the $700,000 to $1 Million range, so let’s focus on the $1M section. Under the “old” tax brackets these people would have crossed into the 39.6% tax bracket starting with their $480,051 dollar. So the first $480,050 was taxed at around 28%, or $134,244. The next $519,950 is taxed at 39.6%, or $205,900. Total Tax under the 2018 “old” tax brackets: $340,144. You can see with our progressive system the first dollars that you make are taxed at a “discount” to the last dollars that you make.

Here is what the proposed 2018 tax brackets would look like:

Your first $600,000 is taxed at about 27%, or $116,998. The next $400,000 is taxed at 37%, or $148,000. So combined the $1,000,000 income is going to be taxed at a total of $309,379, or a tax savings of $30,766. Not enough to hire a new assistant full time, but hopefully enough to send one of your children to college for a year. The government is betting on economic growth, perhaps this tax savings will convince you to upgrade some of your technology. This would be enough to pay for a new office server, new office computers, and 4 K monitors for everyone. However, it isn’t enough of a tax savings to get you a new Conebeam. Although, it would make for a nice down payment on one.

What tax savings would a general dentist expect from the proposed 2018 tax brackets?

Most of appraisals that I do for general dentists show their income from salary and profit between $400,000 and $700,000. Let’s look at a dentist with an income of $424,950. Under the “old” tax rates they would be at the top of the 33% bracket and would pay $114,959 in taxes (progressively around 27%). In the proposed 2018 tax bracket the dentist would be at the bottom of the 35% bracket, but most of their income would have been taxed at about 23% as they progressed up the tax brackets. These dentists are looking at a tax savings of $15,596. Perhaps this year you should add a day of hygiene to your schedule. Maybe it is time to get that digital panorex that you have been putting off.

Aren’t there more aspects to Trump’s Tax Plan?

Is the estate tax/death tax going away? Well no, but they did double the threshold from $5.49 M to $10.98 M. Personally, I’ll lose a bit of business as more and more estates fit into that extra threshold. I’m on board with this change although, I wish it would have gone away completely. The government has already taxed them their entire lives, then they want to tax them another half or so just because they died? I recently wrote an article on the estate tax.

Don’t they phase out certain deductions at certain income levels? Yep, good luck figuring that out!

Isn’t the standard deduction going to go up? Yep for a married couple it will go from $12,700 to $24,000. The good news here is that means that if you currently itemize you may be able to save some time by just taking the standard deduction.

Personal Exemptions go away. OUCH! That was 4,050 per person. So if you have 3 people in your family, the jump up in standard deduction is wiped out. 4 or more people, well let’s just say you aren’t that happy with the plan anymore.

Costal/blue states aren’t going to like that state income taxes are capped at $10,000. Perhaps it’s time to start voting against tax hikes in your states?

Child Tax Credit is going to double to $2,000. This will help take out some of the sting from losing the personal exemptions, that your children otherwise would have had.

Cap on home mortgage deduction from $1,000,000 to $750,000. We will probably see a bit of a dip in prices for houses between $1.2M and about $900,000.

AMT threshold increases from $84,500 to $109,400. This one upsets me the most. I get the idea that we can’t just let people with high income write off everything and pay nothing in taxes. They use the same roads, parks, police, fire stations, bombs, and tanks that the rest of us use. BUT, this plan was supposed to make taxes so easy we could fill them out on a postcard! The AMT is the opposite of a postcard…

The penalty for not having healthcare insurance is gone. I’ll probably do a post or vlog about this at some point. Personally, as a self employed family we have been given the shaft by Obamacare for several years. Our premiums quadrupled, our deductibles tripled. It was like we didn’t even have “coverage” anymore until we had paid something like $30,000 a year. So we moved over to a Christian health sharing plan.

Corporate tax rate is going from 35% to 21%. We need this to compete globally. This one works for me, bring the money back and build your factories here.

Pass Through Businesses, S-corps, LLCs, & Partnerships

Completely against the theme of doing your taxes on a postcard, the proposed changes complicate life so much. Some accountant will come up with the perfect scheme to defeat the idea behind this, so be prepared to pay larger cpa fees in 2018.

So pass through profits are going to go down to a taxable rate of 20%, unless you are in a service business, unless your income is less than $315,000 (married). Complicated enough? See any possible issues or loop holes?

When you run a pass through business you are required to characterize a portion of your profits as salary. That salary has a definition/guidelines as to how much that should be. As an example, let’s say you are a General Dentist and you have $400,000 in profits.

A set up that the IRS wouldn’t like is:

$50,000 in W2 earnings, $350,000 in profits. They would say to this doctor, “so you go to work for 4 days a week and work 9 hour days and you take home around $1,000 a week. Can I hire you to work in the IRS offices?” Nope! You are caught, with your hand in the IRS cookie jar. Prepare for some massive fines.

A split that would likely meet the IRS smell test is:

$250,000 in W2 earnings, $150,000 in profits. Ask yourself, “would I go to work for 36 hours a week at the practice across the street if they gave me $250,000 a year?” Insert the hours you work and change around the dollar amount until you feel like that would be a good deal for you. This number needs to be enough for you to wake up in the morning and go to work for someone else, knowing you no longer have to deal with any ownership responsibilities.

There will be a lot of “gaming of this system”. Seriously, it’s going to be annoying. You have to balance the IRS’s smell test with maxing out your social security, and your ideal:

IRA

Sep IRA

401K

deferred benefit plan

It isn’t going to be a fun situation at all.

Keep in mind that if you are a passive owner in the business, you aren’t going to take a salary at all and are just going to take profits which will be taxed at 20%. Are we going to see massive transfer of companies to kids, and other relatives?

If my son passively owns my business and gets taxed at 20%, then couldn’t he pay me a small salary? My salary would be at normal rates, so as long as my salary is low our family will benefit??? Seriously guys, (Trump, republicans, etc.) how did you dream this up???

What have we learned about the 2018 tax brackets?

The main take away is that the brackets only tell a small portion of the story. Taxes are still complicated so that our government can continue to legislate their agendas through taxation. Were our system different, no lobbyist etc., we could possibly move to a postcard tax form. This tax bill doesn’t get us there, but it feels like a small step in the right direction.

Will it spur economic growth? I’m thinking that they made it so complicated that the main growth will be in the accounting sector. Some of this growth may trickle down into the valuation/appraisal world as I have a feeling we are going to see a lot of asset transfers between family members to game the system.

Half of the people don’t pay taxes, why do they bother with the bottom tax rate?

Don’t get me started on this one. The people at the bottom are hurt the most by tax preparation companies, and their outrageous rapid refund schemes. That is something they should have looked at by giving the people at the bottom of the 2018 tax brackets a chance to fill out a postcard tax return. This was a complete miss by the republicans.

Ross Landreth provides valuation services, you should not take any of this information as tax or legal advice.

All appraisers are required to follow the Uniform Standards for Professional Appraisal Practice (USPAP). Think of this as the check list that appraisers need to follow for every assignment. Appraisers in the business valuation field need to take a 7 hour USPAP class every 2-5 years, while real property appraisers need to take the 15 hour USPAP class to enter the field. We know that it takes a JD to become a lawyer, an MD or a DO to become a doctor. What does it take to become a qualified appraiser?

First, let’s go with the IRS definition of a qualified appraiser. An IRS qualified appraiser is an individual who:

Has earned an appraisal designation from a recognized professional appraisal organization, or has met certain minimum education and experience requirements.

Regularly prepares appraisals for which the individual is paid.

Demonstrates verifiable education and experience in valuing the type of property being appraised.

Has not been prohibited from practicing before the IRS in the last three years

Is not an excluded individual.

If you are looking for the requirement for real estate appraisers just click the third option on the menu to skip the business valuation information.

There are several competing organizations which have different sets of rules to join their ranks and become certified/qualified as an appraiser. I’m going to focus on the ones that are recognized by the SBA. All of these require at least a bachelor’s degree and many hours of initial training and experience.

SBA definition of a Qualified Appraiser

The Small Business Administration has criteria for who they allow to perform appraisals for underwriting SBA loans. There are a few appraisal designations that are left out of their qualified list, which should be a clear signal that these are the only business valuation credentials which should count.

Accredited Senior Appraisers (ASA) from the American Society of Appraisers

Certified Business appraiser (CBA) from Institute of Business Appraisers

Accredited business valuation (ABV) from AICPA

Certified valuation analysts (CVA) National Association of CVA’s

Let’s look into the requirements to earn these credentials.

*I didn’t realize this until I went to look at CBA requirments, but they were purchased by NACVA. Which means that as the re-certification process occurs the CBA designation will be phased out. For the last decade or so no new CBAs should have been awarded.

I had appraised insurance agencies and dental practices for many years before I started the course work to get an ASA. I knew that I could only go so far without a credential, I needed to basically be “under” someone in the corporate ladder. Someone had to sign and supervise my work. Had I been hungrier to move up the food chain I would have started on my formal appraisal education sooner. Was I lazy? Or did I just not know what I didn’t know?

I have to chalk this up as I just didn’t fully understand what I didn’t know. My company was unwilling to pay for me to take the courses. It wasn’t until I went out on my own that I started to invest in myself. The four 26 CE hour courses aren’t cheap. They require travel, and a few days off work for each of the modules. Here is another tip the first two exams are easy, the next two are much more difficult. So be prepared to study!

What benefits do Credentialed Appraisers Have?

It is a huge perk to be able to do SBA work for banks. I generate about 20% of my business from banks and that’s revenue that I would hate to lose. My five year re-accreditation window is fast approaching, and believe me I’m going to jump all of the ASAs hoops to ensure I don’t lose out on SBA work.

Having a business appraisal credential gives you a measure of respect. Many potential clients do their research before they hire an appraiser. Ask yourself, after a short google search are you more likely to hire someone with a business valuation credential than someone without? Assume that the valuation assignment is the same cost, then you aren’t going to go to an untrained person when you could just hire a certified one.

Knowing that the ASA’s requirements are more difficult than the other organizations, I chose to go down that road. The main reason behind my decision? I didn’t want to walk into court and have a resume that was deemed inferior to the other party’s expert witness. Being armed with an ASA makes it easy to qualify as an expert witness. Of course, you need to get one case under your belt before attorneys will take the risk and hire you for their assignment.

I imagine that all judges, mediators, and arbitration panels know the difference between a credentialed appraiser and one without qualifications. However, arguing that an ASA is more important than say a CVA most likely won’t be worth the effort. I know that the ASA is more prestigious and difficult to attain, but I’m not going to bust out a chart and tell the judge that the other guy isn’t qualified to sit in the same chair as I am.

However, I do get a nice chuckle when I’m in court against a broker and the judge asks him about his business valuation training and experience. Rather than trying to outshine the other side, just sit back and let them explain their lack of experience. In the end, the judge will understand that the other party brought a knife to a gun fight.

Qualifications for Real Estate Appraisers

The real estate world is heavily regulated so the requirements are straightforward. From time to time requirements may be changed by the AQB (Appraiser Qualification Board). There are three levels of certification; licensed residential, certified residential and certified general.

To get started you need to become a trainee appraiser. You will need to find someone to take you under their wing and show you the ropes so that you can get the hours needed to progress through the ranks.

Trainee Appraiser

CE Hours

Basic Principles & Procedures

60

15 Hour USPAP

15

Total Hours

75

As you can imagine if you want to progress through the ranks and appraise larger properties and commercial properties you will need to put in more class room time. As a trainee you are expected to keep a log book of the properties that you appraise.

Time to move on to the next level:

Licensed Residential Real Property Appraiser

This will allow you to appraise residential units with values up to $1,000,000.

Licensed Residential

CE Hours

Trainee Requirements

75

Residential Market Analysis

15

Residential Site Valuation

15

Residential Sales Comparison & Income Approach

30

Residential Report Writing

15

Total Hours

150

In addition to the 150 hours of continuing education required to progress this far, one needs to also have 30 hours of college courses under their belt. This roughly translates to about a year of college at 15 units per semester. So if you have an associate’s degree or a bachelors degree you can cross this off your list. As a trainee you also need to put in 2,000 hours of experience in the last year. Which means that if you weren’t a full time trainee appraiser during the last year, you won’t be able to progress.

The final requirement needed to attain the licensed residential real property appraiser designation is to pass the AQB approved examination.

If you have attained a bachelor’s degree you can progress to the next level:

Certified Residential Appraiser designation

This gives the appraiser the ability to appraise residential units without regard to complexity or value. They are also allowed to appraise vacant or unimproved land that may be used for residential units in the future.

To progress this far you will need the following CE courses.

Certified Residential

CE Hours

Trainee Requirements

75

Residential Market Analysis

15

Residential Site Valuation

15

Residential Sales Comparison & Income Approach

30

Residential Report Writing

15

Statistics, Modeling & Finance

15

Residential Case Studies

15

Appraisal Electives

20

Total Hours

200

You can see that you need to put in an additional 50 CE hours, and you need to be in the appraisal field for 2 years (minimum 2,500 hours).

With another six months of on the job training in the commercial appraisal field you can progress to:

Certified General Real Property Appraiser

It’s not much of a leap, an additional six months and 100 CE hours, but this step up on credential allows you to appraise all types of real property. That’s right, you are now free to do all the things that you have learned, nobody is holding you back. Just follow USPAP and do what you do best.

Certified General

CE Hours

Trainee Requirements

75

General Appraiser Market Analysis

30

Statistics, Modeling & Finance

15

General Appraiser Sales Comp Approach

30

General Appraiser Site Valuation and Cost Approach

30

General Appraiser Income Approach

60

General Appraiser Report Writing

30

Appraisal Electives

30

Total Hours

300

Something that I didn’t mention is a new rule for 2017; the background check rule:

All applicants for a real property appraiser credential shall possess a background that would not call into question public trust.

Applicants shall provide state appraiser regulatory agencies with all of the information and documentation necessary for the jurisdiction to determine the applicant’s fitness for licensure or certification.

An applicant shall not be eligible for a real property appraiser credential if, during at least the five year period immediately preceding the date of the application for licensing or certification, the applicant has been convicted of, or pled guilty or nolo contendere to a crime that would call into question the applicant’s fitness for licensure

Additional guidance related to background checks for applicants for a real property appraiser credential may be found in Guide Note 9 of TAF_2017_appraiser guide

An appraiser has access to numerous properties. It makes sense that the AQB has the ability to reject people with criminal records. This helps to restrict this access to people who have been on the correct side of the law.

If you have a medical license you are in luck. Banks are aggressively pursuing this portfolio and will compete to get your business.

Wells fargo’s practice finance division in Emeryville CA (was matsco years ago)

Bank of America has a practice solutions division

Both of those banks loan on the current cash flow of the business you are looking at; so if it doesn’t have cash flow you aren’t going to get a loan

Good credit scores are a must 700+

They offer start up financing of around $600,000 if you want to start from scratch

Check with the bank that currently handles the practice’s deposits

I tend to stay away from banks that have what I call “branch authority”. Sometimes branches of large banks have the ability to loan at the branch level, the problem with this is that the manager also approves loans for sandwich shops, and car washes. So this loan officer won’t have a streamlined process to get you in and out of the system (you are treated like anyone else). Here is this conversation in a video that I just shot.

Bad Credit, but you have a medical license:

Be prepared to hear no a lot. You will be forced into 3 options if you have bad credit:

Find a bank broker (I know a few people who shop loans to various banks)

SBA (under 7.5M in revenue for Dentists and Optometrists)

Seller Financing

No medical Degree:

SBA has a huge book called the sop, in it they have a table of what it takes to remain small:

Liquor stores, drinking places, full service restaurants, barber shops, beauty salons under $7.5M

Let’s talk about the SBA 7(a)

Run and backed by the government. So the bank that loans you the money gets to transfer the risk of the loan to the government. The govt takes the loan the bank gets credit for “selling it” and they will collect the payments. For the government to take this deal the bank needs to jump through all of the hoops in the SOP book.

Is it over $250,000 in value (not including real estate)? You need an appraisal

Are family members involved? If yes you need an appraisal

The appraiser must be hired directly by the lender, and the report prepared specifically for the lender.

Who can appraise the business for an SBA loan?

A broker did an appraisal surely that’s good enough right? NOPE SORRY!

The government only accepts qualified appraisers so:

CPAs

Accredited Senior Appraisers (ASA) from the American Society of appraisers (I have this designation)

Certified Business appraiser (CBA) from Institute of business appraisers

Accredited business valuation (ABV) from AICPA (this also requires a CPA)

Certified valuation analysts (CVA) national association of CVA’s

If this part wasn’t clear, you need to pay for an additional appraisal to use SBA financing. Even if you had a qualified appraiser prepare the valuation you used to negotiate the purchase, the bank needs a separate one for their paperwork. As an appraiser, I’m not allowed to just change the name of the client from you to the bank. I don’t need to start from scratch, but I need to start a new file and work through it as if the bank was a brand new client. Fortunately when it comes time to crunch the numbers, well that parts already done.